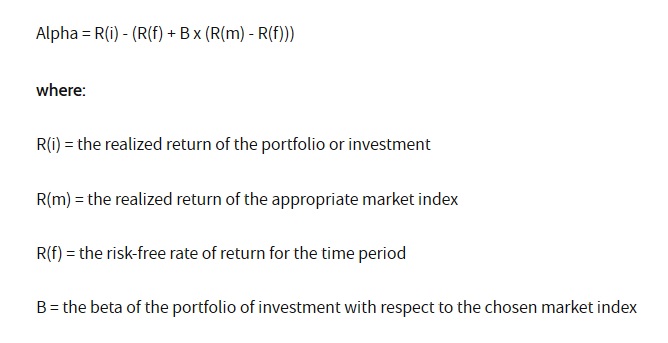

Jensen's alpha, is a risk-adjusted performance measure that represents the average return on a portfolio or investment, above or below that predicted by the capital asset pricing model (CAPM), given the portfolio's or investment's beta and the average market return. (Market return: NASDAQ 100 index)

jensen alpha