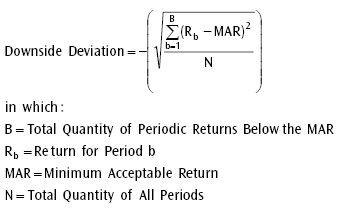

Downside deviation is a measure of downside risk that focuses on returns that fall below a minimum threshold or minimum acceptable return (MAR). It is used in the calculation of the Sortino Ratio, a measure of risk-adjusted return.

downside deviation